A maximum offset of $540 is available to taxpayers making non-deducted superannuation contributions on behalf of a spouse.

A spouse of a person includes another person (whether of the same sex or a different sex) with whom the person is in a registered relationship (prescribed for the purposes of s22B of the Acts Interpretation Act 1901), or another person who, although not legally married to the person, lives with the person on a genuine domestic basis in a relationship as a couple.

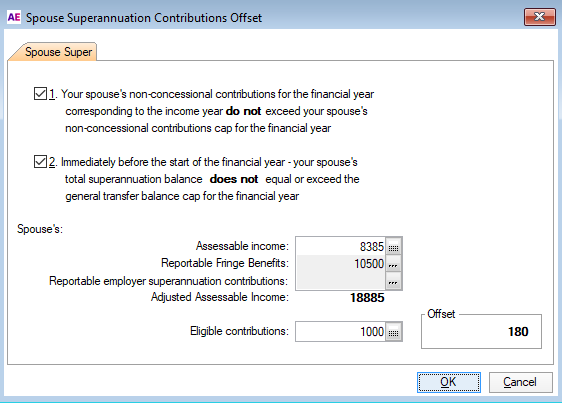

The taxpayer is eligible if:

-

the contributions were non-deductible to the claimant

-

both the taxpayer and spouse were Australian residents at the time the contributions were made

-

both the taxpayer and spouse were living together permanently at the time the contributions were made

-

the sum of the spouse's assessable income plus reportable fringe benefits and reportable employer superannuation contributions for the year was less than $40,000

-

spouse’s non-concessional contributions for the financial year corresponding to the income year do not exceed the spouse’s non-concessional contributions cap for the financial year

-

immediately before the start of the financial year, the spouse’s total superannuation balance does not equal or exceed the general transfer balance cap for the financial year.

To complete the Contributions on behalf of Spouse worksheet

Click label A at item T3 to open the worksheet.

Answer the eligibility questions and enter the details.

The offset is calculated as 18% of the lesser of:

-

$3000, reduced by $1 for every $1 that the spouse’s assessable income and total reportable fringe benefits amounts for the year was more than $37,000 and less than $40,000, or

-

the total of the contributions made by the taxpayer for the spouse.

When you close the worksheet, we'll pass any offset calculated to Item T3: label A.