The ATO has made no provision in the Partnership return for the ESVCLP tax offset to be distributed to the partners.

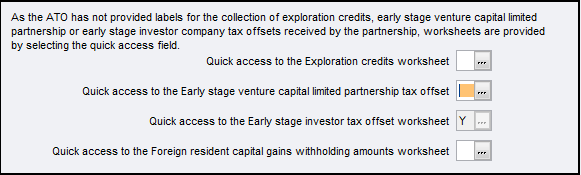

We've provided some MYOB only Quick Access fields at item 51 so that you can distribute any ESVCLP tax offset earned by the partnership or received as a share of distribution from another partnership or trust to the partners.

Before claiming the ESVCLP tax offset, it's important to read the ATO information Tax incentives for innovation.

Click in Goto (F2) and enter 51 and press Enter, or click the Distribution tab to move to item 51: Statement of distribution:

Example 1: Partnership invests in an ESVCLP

In this example the partnership has already claimed the Early stage Investor tax offset.

-

Enter Y at the Quick access to the Early stage venture capital limited partnership tax offset field to open the ESVCLP tax offset worksheet esv.

-

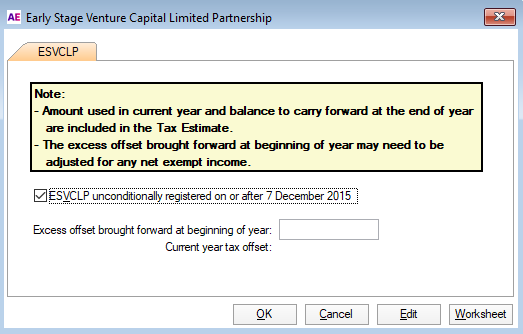

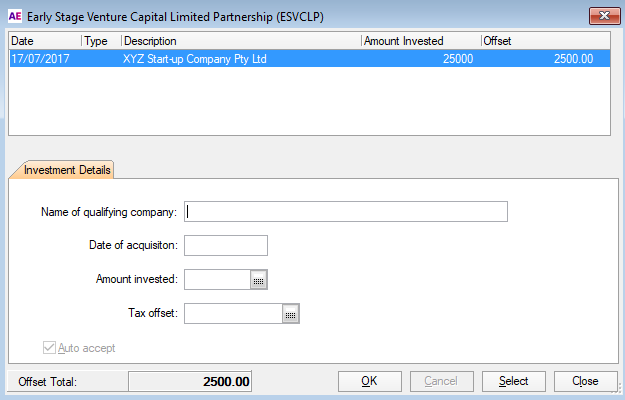

Click the Worksheet button and enter the details of the acquisition of shares in the ESVCLP.

-

Enter any Excess offset brought forward from the previous year, adjusted under Div 65 of the ITAA 1997 for the effects of any net exempt income (foreign or Australian).

-

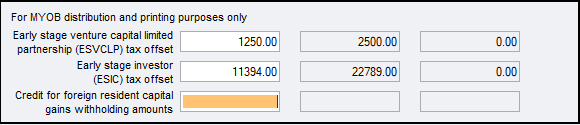

We'll pass the Offset total to the special fields in the Distribution statement worksheet xP for distribution to the partners.

-

Sharing occurs by pressing F8 from the main return or clicking the Distribute button at item 51. When shared we'll create a Distributions from partnerships worksheet (dip) in each partner's return.

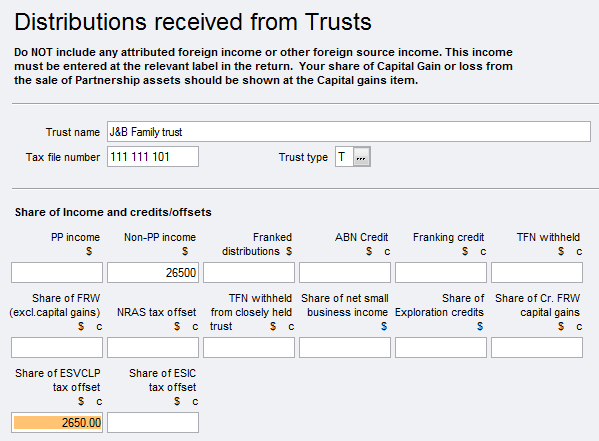

Example 2: Partnership receives a share of ESVCLP tax offset from a trust

The share of ESVCLP tax offset entered in either of the Distributions from partnerships or Distributions from trusts worksheets at item 8 is passed to the esv worksheet as an entry recognised by the Type code D.

There is no F4 estimate for the partnership as the share of the offset is claimed by each partner in their own tax returns.

CCH References

20-700 Outline of innovation incentives