Release date—2 April 2019

Compliance

Inland Revenue (IR) transformation project

As part of the IR transformation project, IR are changing the back-end processor for E-File.

E-File is a way for tax agents to transmit data from software directly to IR. It's the most significant channel for the submission of income tax returns, typically used for about 75 per cent of all returns filed.

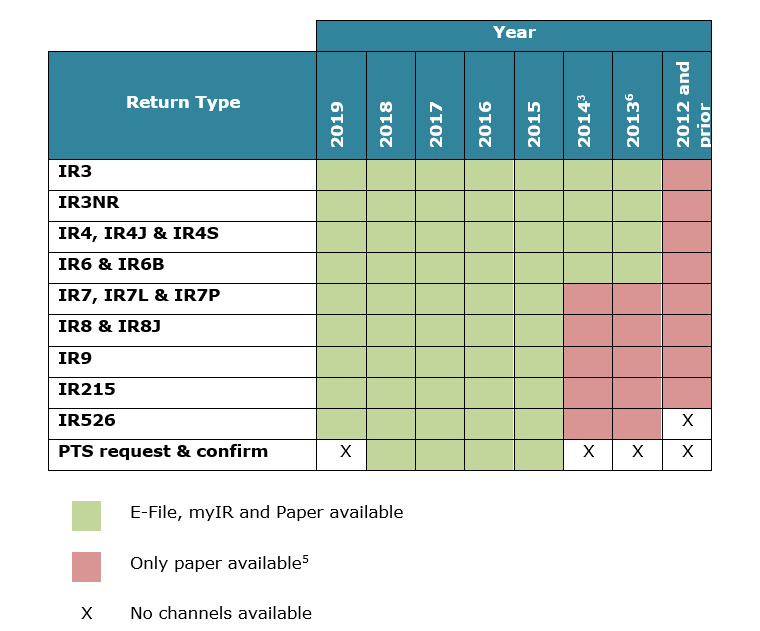

E-File accepts the following return types and attachments:

-

IR3—Individual Income Tax Return

-

IR3NR—Non-Resident Income Tax Return

-

IR4/J/S—Companies Income Tax Return

-

IR215—Adjust your income

-

IR526—Donation Tax Credit Claim Form

-

IR833—Property sale information

-

IR6/B—Estate or Trust Income Tax Return

-

IR7/L/P—Partnerships and Look-Through Companies (LTCs) Income Tax Return

-

IR8/J—Maori Authorities Income Tax Return

-

IR9—Clubs or Societies Income Tax Return

-

IR10—Financial statements summary

-

IR101—Goods & Services Tax Return

-

Personal tax summaries

-

Correspondence.

If you're an agent, you can also receive your client lists, debt letter reports and summary of earnings reports, as well as notices produced as a result of filing (notice of assessment, return acknowledgement and notice of entitlement).

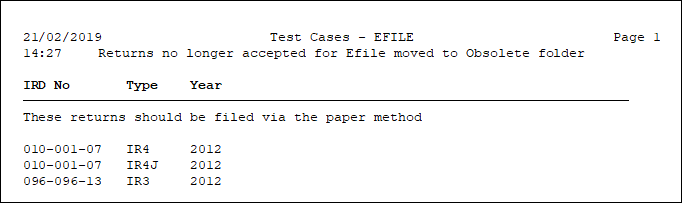

You won't be able to E-File tax returns for 2012 or earlier, and some return types from 2013 will be affected. You can create returns in AO Classic Tax for all affected years, and you can print and send the C-Series report to IR.

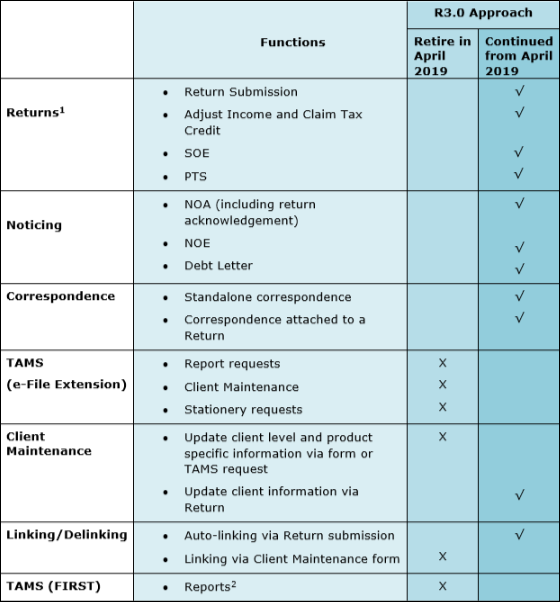

Function changes

You can create returns in AO Tax for all affected years, and you can print and send the C-Series report to IR.

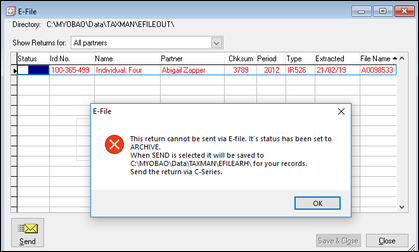

When you lodge the return via the E-File system, the return won't be sent to IR and the file will be moved to C:\MYOBAO\DATA\TAXMAN\EFILEARH\ as a record.

Returns that won't be sent via E-File are indicated by a red table row entry.

You can run a report that shows you the returns that are in the EFILEARH folder and the date that the files were moved. Run the report from E-file > Reports > View list of returns in E-File Archive folder.

Updates of status, dates and amounts will continue to flow to Tax Tracking and Tax Manager as usual, but you won't receive notices or assessment details from IR.

Best Start Tax Credit (BSTC)

A new Best Start Tax Credit is a payment of up to $3,120 per year (or $60 per week) per qualifying child.

BSTC applies to children born on or after 1 July 2018.

BSTC will be available to all families in the first year of a child's life. For the second and third year, for families with income over $79,000, the credit will be abated at a rate of 21 cents per dollar of income.

If you're claiming Paid Parental leave (PPL), you can't claim BSTC at the same time. BSTC will start when PPL has finished.

The rules for calculating BSTC are in section MG2 of the Income Tax Act. Section MG2 (1) defines the calculation as prescribed amount × days ÷ 365. As the credit is only available from 1 July 2018, the maximum number of days entitlement for the 2019 year will be 274. The prescribed amount is $3,120.

If a child dies during the year, the entitlement period is extended for 4 weeks (28 days) after the date of death.

Examples

-

A family has one child born on 29 June 2018.

-

There's no BSTC entitlement, because it only applies to children born on or after 1 July 2018.

-

-

A family has one child born on 31 July 2018.

-

In 2019, BSTC will apply for 244 days, and will be $3,120 × 244 ÷ 365 = $2,085.70.

-

In 2020, BSTC entitlement will depend on family income. The full BSTC amount will apply from 1 April 2019 until a child's 1st birthday on 31 July 2019 (122 days), after which the entitlement will be abated at a rate of 21 cents per dollar for every dollar of family's income over $79,000.

-

-

A family has twins born on 1st November 2018.

-

-

In 2019, BSTC will apply for 151 days, and will be $3120 x 151 / 365 = $1,290.74 x 2 children = $2,581.48.

-

Working with Best Start Tax Credit

-

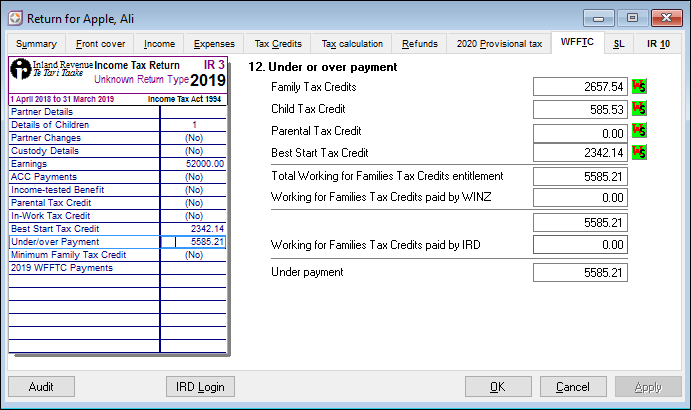

To display Best Start Tax Credit, click the WFFTC (working for families tax credit) tab. The Best Start Tax Credit amount is displayed in the Under or over payment section.

-

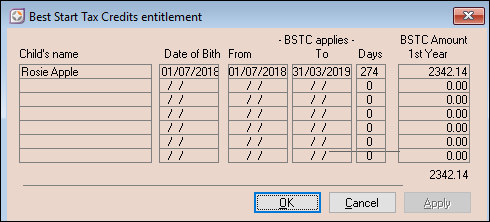

Click the worksheet icon next to the Best Start Tax Credit amount to display the details.

-

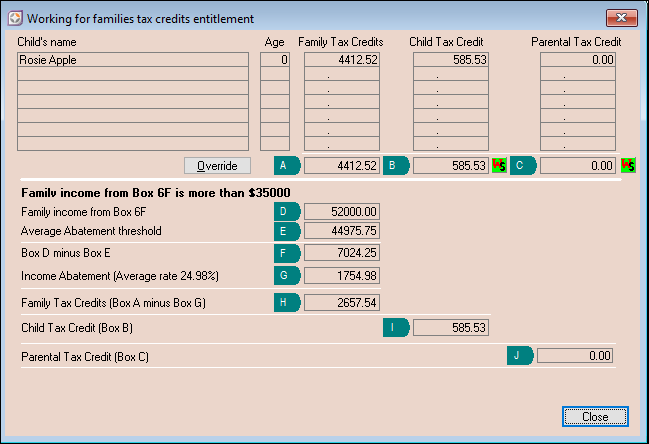

Click the worksheet icon next to the Family Tax Credits amount to display the details. The abatement rate is broken into 2 periods, so the Average Abatement threshold and Income Abatement display as average rates.

-

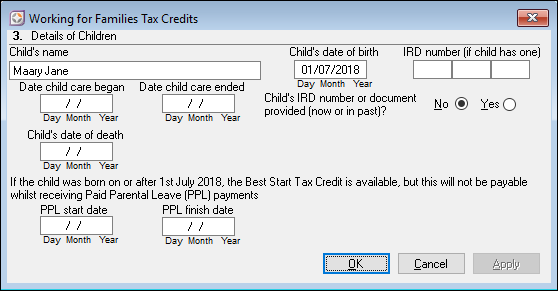

Enter the child's details in the table to the left.

-

If you need to enter Paid Parental leave (PPL) or the date of death:

-

Double-click the table on the left. The Working for Families Tax Credits window appears.

-

Enter the details and click OK.

-